Introduction

Most small business owners know their revenue. Many, I'm hoping, their profit. But very few can tell you their cash position on any given day, and no, this is not your current bank balance!

A closer look into small businesses' finances often draws one conclusion: that a business that is profitable on paper is running out of money in practice. The business is not failing. The finances just have a structural problem that no one has named yet.

After reading this post, you will understand the difference between cash flow and profit, why both matter, and what to do when they are telling you different stories about your business.

What Is Profit?

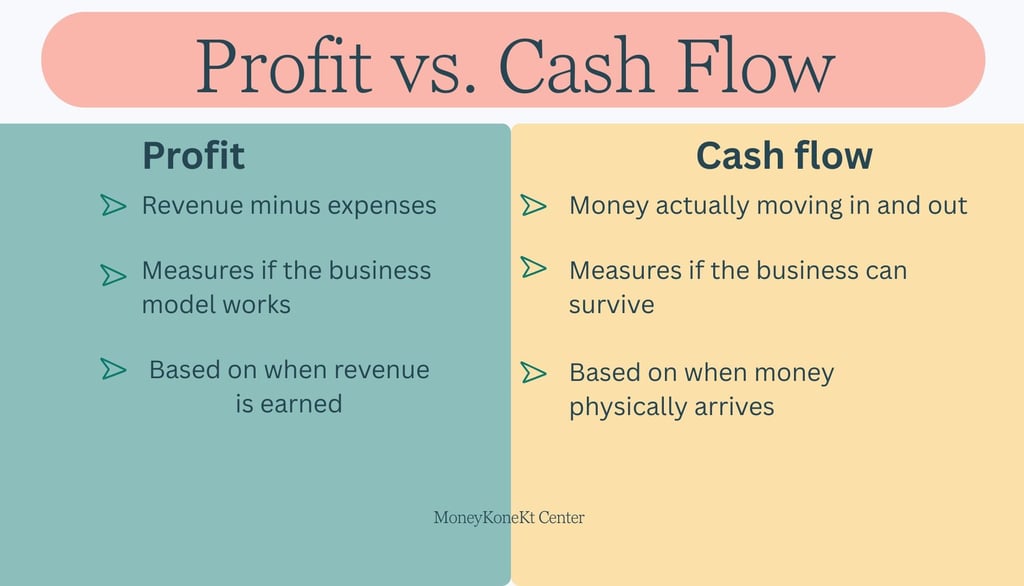

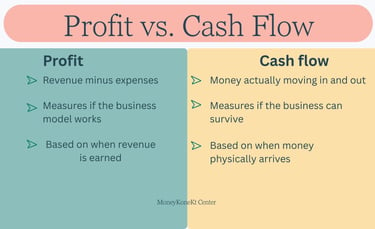

Put simply, profit is what is left after you subtract your expenses from your revenue.

Profit example: If your business brings in $10,000 in a month and your total costs, e.g. staff, rent, supplies, utilities, are $6,000, then your profit is $4,000

Profit is a snapshot of whether the business is commercially viable. Are you earning more than you spend? Profit answers that question.

There are two types of profit:

Gross profit: This is revenue minus the direct costs of making and/or delivering your product or service(what accountants call the cost of goods sold). If you ran a small restaurant, gross profit is what is left after the cost of food and kitchen staff.

Net profit: This is what remains after all costs, including rent, admin, loan repayments, and every other overhead, have been deducted. This is probably what you think of when you think of profit and what matters, just to keep it simple and easy to remember. ,

Profit lets you know whether your business model is working, but it does not tell you whether you have money.

Okay, so what is Cash Flow?

Cash flow is the movement of actual money in and out of your business account over a given time period.

It is not what you have earned. It is the money that has actually arrived and what has actually left.

If you invoice a client $8,000 today, that amount appears in your revenue and contributes to your profit calculation at the end of the day. If the client pays in 45 days, you do not have $8,000 in your account today. You have a receivable, a promise of money. So you can imagine if you need to pay an electricity bill today...on paper, profitable, but no money.

Cash flow tracks the real-time reality: when money comes in, when it goes out, and what is left.

Positive cash flow means more money is arriving than leaving in a given period. Your business can pay its bills, its staff, and its suppliers without stress.

Negative cash flow means more money is going out than coming in. Even if you are profitable overall, negative cash flow in a given month means you may not be able to meet your obligations.

Cash Flow vs Profit: The Key Difference

The simplest way to understand the difference is this: profit is what you earn on paper. Cash flow is what actually moves in and out of your bank account.

Profit is calculated based on when revenue is earned and when expenses are incurred, regardless of when money actually moves. Cash flow only counts money that has actually moved.

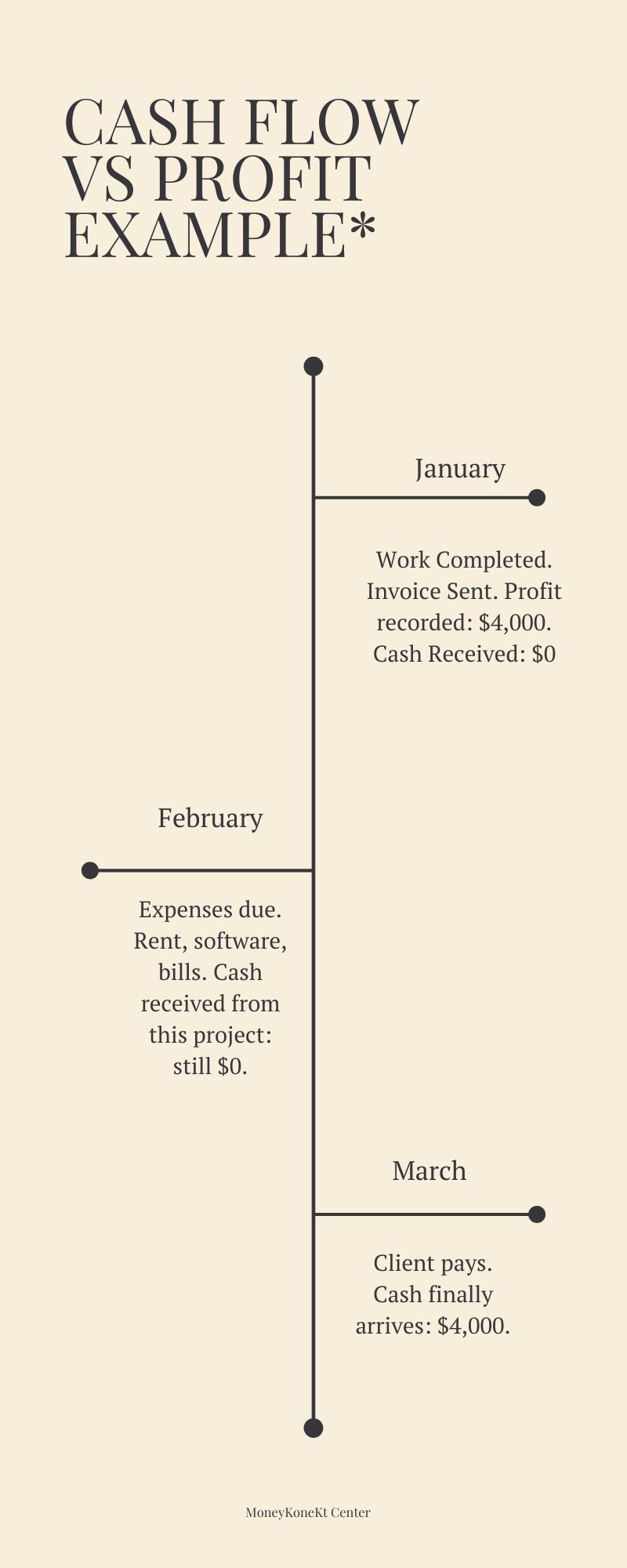

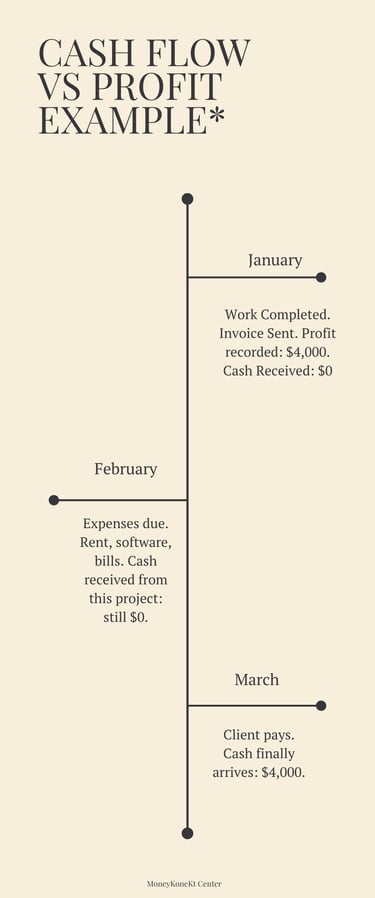

Here is an example:

A freelance web designer completes a $4,000 project in January. She invoices the client on completion. The client pays 45 days later, in mid-March.

In January, her profit statement shows $4,000 in revenue. Her business looks profitable.

But in February, that $4,000 has not arrived. Her cash flow for February shows nothing from that project. Rent is due. Software subscriptions are due. If she does not have a buffer, she has a problem, despite running a profitable business.