How to Separate Your Personal and Business Finances (Step-by-Step)

Learn how to separate your personal and business finances in 7 clear steps. Avoid costly tax mistakes, track expenses properly, and protect your business

Dennis Muchemi

4/4/202610 min read

Most small business owners mix their personal and business finances in the beginning. It feels harmless at first: it's just a $20 electricity bill, or a $10 lunch for your staff, you pay a supplier from your personal account, deposit a client payment into your personal savings, buy office supplies on your personal card. No big deal, right?

Until tax season arrives. Or a client asks for an invoice history. Or you try to figure out whether your business actually made money last month.

That is when mixed finances stop being a minor inconvenience and start costing you real time, real money, and real stress. In this guide, you will learn exactly how to separate your personal and business finances in seven clear steps, including what to do if your finances are already mixed.

Why you need to separate your personal and business finances

Before we get into the steps, it is worth being clear on what is actually at stake. This is not just a good-to-have habit. It is the foundation of every other financial decision you will make in your business.

Tax clarity and legal protection

When your personal and business transactions are in the same account, every expense becomes a guessing game at tax time. Which purchases were for the business? Which were personal? Without clean records, you risk either missing legitimate deductions or claiming personal expenses incorrectly, both of which can attract unwanted attention from HMRC, the IRS, the ATO, KRA or whichever tax authority applies to you.

If your business is a registered company (an LLC, Ltd, Pty Ltd, or similar), the legal separation between you and the business only holds up if you treat them as genuinely separate. Mixing finances, a practice accountants call commingling funds, can weaken that separation and, in serious cases, expose your personal assets to business liabilities.

Cash flow visibility

You cannot manage what you cannot see. If your business income and expenses are tangled with personal transactions, there is no reliable way to know whether your business made or lost money in a given month. You will likely feel like money is disappearing without being able to identify where.

Clean separation gives you the ability to read a simple bank statement and immediately understand the financial health of your business. That visibility is what lets you make decisions: when to hire, when to cut costs, when to invest.

Credibility with banks, lenders, and clients

If you ever apply for a business loan, grant, or line of credit, lenders will ask to see your business financials. Mixed accounts make this process significantly harder. Some lenders will decline applications that cannot show clean business-only records.

Beyond lending, professional separation signals credibility. It is the difference between a business and a hobby, and clients, partners, and suppliers notice.

Can I use my personal bank account for my small business?

Technically, in most countries, you can - but you shouldn't.

For sole proprietors and sole traders, there is usually no legal requirement to hold a separate business bank account. However, using a personal account for business transactions creates a bookkeeping and tax nightmare that becomes increasingly costly to untangle as your business grows. The admin time alone is rarely worth the short-term convenience.

For registered companies, LLCs, limited companies, corporations, and their equivalents, mixing funds is more than inconvenient. The legal separation between you and the entity requires financial separation too. Most business structures formally require the business to hold its own account, and failing to maintain this distinction can have real legal consequences.

The short answer: even if your business structure technically allows it, a separate account is worth opening from day one.

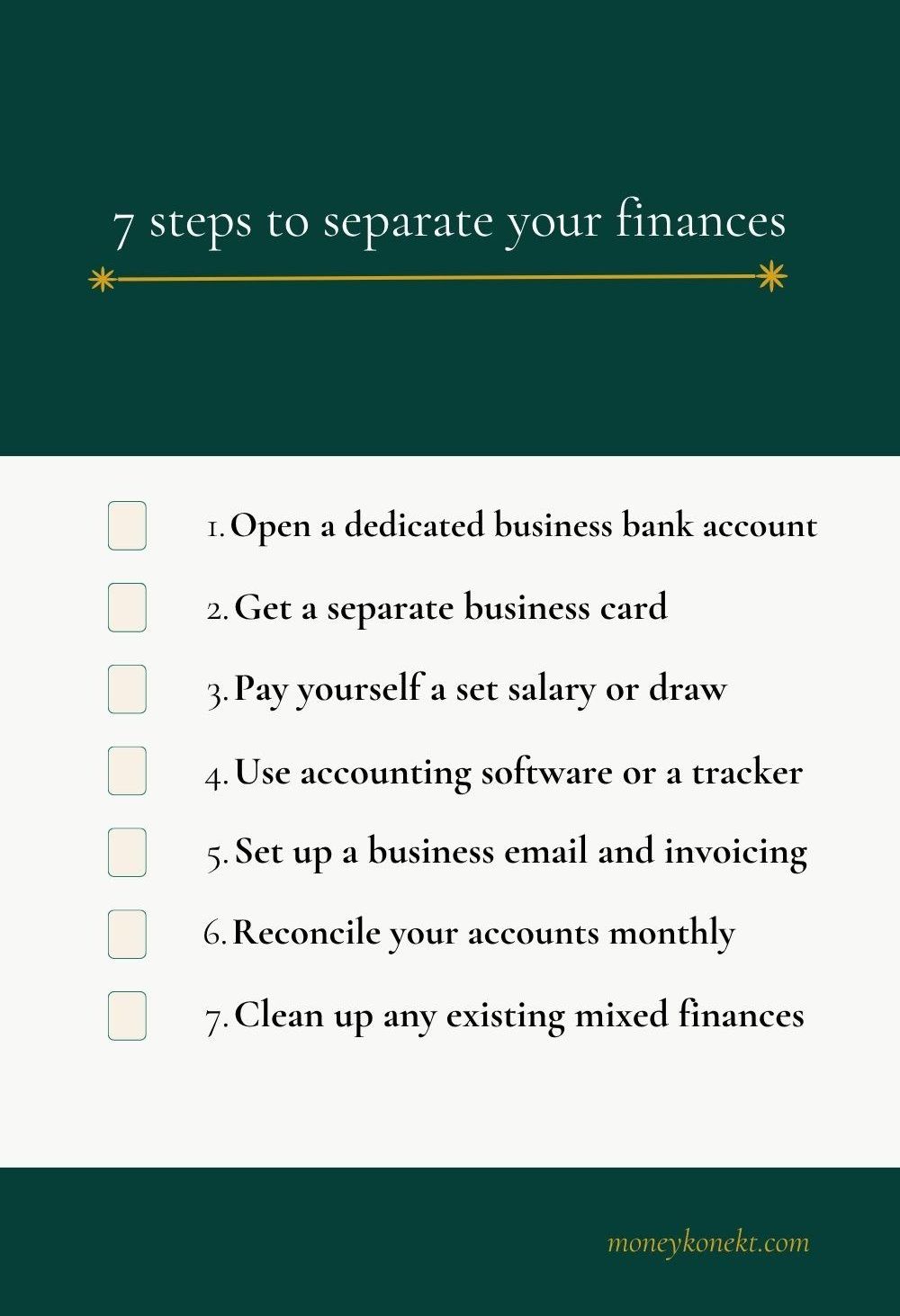

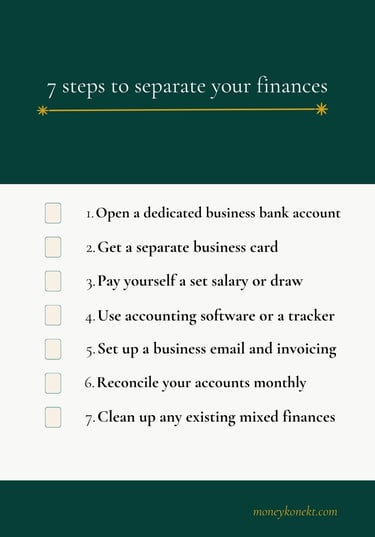

How to separate your personal and business finances (7 steps)

Step 1: Open a dedicated business bank account

This is the single most important step. Everything else follows from it.

A dedicated business account means every business transaction, whether income or expense, runs through one place. You have a clean record of what the business earned and spent, and your personal finances are completely untouched.

Most major banks offer business accounts at low or no cost for new small businesses. In the US, options like Mercury, Relay, or Bluevine offer free business checking with no minimum balance. In the UK, Starling, Monzo Business, and Tide offer free business accounts with useful bookkeeping integrations. In Australia, Up Business and ANZ Business provide options worth comparing. In Canada, RBC, TD, and Scotiabank all have entry-level business accounts, and challenger banks like Relay are expanding there too.

When opening your account, use your registered business name. If you are a sole trader or sole proprietor operating under your own name, you can still open a business account; most banks accommodate this. Bring your business registration documents if you have them, and check whether the bank requires a minimum opening deposit.

Once the account is open, all client payments go in. All business expenses come out. That is the rule from this point forward.

Step 2: Get a separate business credit or debit card

A dedicated card for business spending does two things. It makes your expense records automatic; every transaction is captured without you having to manually sort through a personal statement. And it makes it nearly impossible to accidentally pay for something personal from the business, or vice versa.

If your business bank account comes with a debit card, start there. You do not need a business credit card to start, but if you want one, it can be useful for managing cash flow on business expenses and building a credit history for the business. Just treat it like any credit card, pay the balance in full each month to avoid interest charges becoming a hidden cost.

Physically label the card if it helps. Some business owners write "BUSINESS ONLY" in marker on their personal card as a reminder to reach for the right one.

Step 3: Pay yourself a defined salary or owner's draw

This is the step that most business owners skip, and it is often the root cause of ongoing financial mixing.

If you treat the business account as an extension of your personal wallet, dipping in whenever you need money, you will never have a clean picture of what the business actually costs to run or what it earns. Every personal withdrawal distorts the numbers.

The solution is to pay yourself deliberately and consistently. There are two common approaches:

Owner's salary: You transfer a fixed amount to your personal account on a set date each month, just as an employer would pay you. This works well for businesses with stable, predictable revenue.

Owner's draw: You transfer a percentage of profit at regular intervals, monthly or quarterly. This is more flexible and works better for businesses where revenue fluctuates significantly.

The specific amount matters less than the consistency. Decide on an amount or percentage that covers your personal needs, and stick to it. When you need more money personally, you increase the draw deliberately rather than dipping into the account at random.

Step 4: Use accounting software or a dedicated spreadsheet for business expenses only

Tracking your transactions is what turns a separate bank account into actual financial visibility. Without a system, you still have no idea where the money went; it is just isolated in a different account.

You do not need expensive software to start. Free options like Wave (excellent for US, Canada, and UK-based small businesses) let you connect your business bank account directly and categorise transactions automatically. Xero and QuickBooks are more feature-rich options for businesses that need stronger reporting. Both are widely used in Australia, the UK, and the US, and both charge a monthly subscription fee.

If you prefer a spreadsheet and are not ready for software, a simple Excel or Google Sheets tracker with columns for date, description, category, income, and expense covers the basics. The important thing is that this tracker only ever contains business transactions, not a mix.

Whatever system you use, link it to your business bank account and your business card. The goal is that every business transaction flows into one place automatically, so your records are always current without a weekly manual entry session.

Step 5: Set up a separate email address and invoicing system for the business

Finance separation is not just about bank accounts. The paper trail matters too.

A dedicated business email address does several things: it keeps business correspondence out of your personal inbox, it looks professional to clients, and it ensures that invoices, receipts, and supplier emails are all in one retrievable place when you need them at tax time.

Your invoicing should also be separate. If you are invoicing clients directly from a personal email using a manually typed document, you have no reliable record of what was sent, when, or whether it was paid.

Free invoicing tools like Wave, Zoho Invoice, or even a simple PDF template sent from your business email address solve this immediately. The key requirement is that every invoice is numbered sequentially, dated, and saved somewhere you can find it. Your tax authority in almost every country requires you to keep business records for at least five years; the exact period varies, but five years is a safe standard to apply globally.

Step 6: Reconcile your accounts at least once a month

Opening a separate account and tracking expenses is not enough on its own. You need to check the numbers regularly to make sure everything is accurate and nothing has slipped through.

Reconciliation means comparing your accounting records against your actual bank statement to confirm they match. It is the step that catches a personal expense that accidentally went through the business card, a client payment that did not get recorded, or a subscription you forgot was still running.

This does not have to take long. For most small businesses in the early stages, a monthly reconciliation takes 20 to 30 minutes. You sit down with your bank statement, compare it against your expense tracker or accounting software, and flag anything that does not match.

If you want to make this easier, build a simple monthly finance review habit. Block 30 minutes at the end of each month, pull your statements, and check the numbers. You will catch problems early instead of discovering them at year-end when they are much harder to fix.

For a deeper look at tracking your business cash flow accurately, read: [How to Track Your Business Cash Flow (Without an Accountant).]

Step 7: What to do if your finances are already mixed

If you are reading this guide having already run your business with a single account for months or years, you are not starting from zero. But the separation process is not complicated; it just requires a one-time cleanup.

Here is how to approach it:

Start clean from today. Open your business bank account now and direct all future transactions through it. Do not wait until you have untangled the past before moving forward.

Work backwards through the last 3 months. Pull your personal bank and card statements for the last 90 days. Go through each transaction and label it clearly: business or personal. Most accounting software and bookkeeping tools let you import bank statements as a CSV file and categorise transactions in bulk, which speeds this up considerably.

For older transactions, decide how far back matters. Your tax authority will set the formal requirement, but practically speaking, focus your energy on the current tax year. Anything older than 12 months is worth reviewing only if you are preparing back-dated tax returns or resolving a specific discrepancy.

Log any business expenses paid from personal funds. These are legitimate business costs and may be deductible. Record them in your bookkeeping system as owner contributions or out-of-pocket business expenses. An accountant or bookkeeper can help you categorise these correctly if you are unsure.

Once the cleanup is done, the separation going forward takes care of itself -- because the infrastructure you have built in steps 1 through 6 prevents the mixing from recurring.

Want to know exactly how your business finances stack up across all five key areas?

The MoneyKoneKt Business Finance Health Check walks you through 20 questions covering cash flow, bookkeeping, profitability, tax, and financial visibility. It takes 10 minutes, it is free, and it tells you precisely where to focus first.

Frequently asked questions

Should I use the same bank for my personal and business accounts?

You can, but there is a practical reason to consider different banks: it reduces the temptation to transfer money between accounts casually, which is where mixing often starts again. That said, using the same bank can simplify transfers when you need to pay yourself your salary or draw. The more important point is that the accounts are separate; whether they sit at the same institution is secondary.

How do I separate my finances as a sole trader or sole proprietor?

The process is identical to the steps above. The legal structure does not change the practical approach. Open a business bank account in your own name designated for business use, route all business transactions through it, pay yourself through a regular transfer, and track your business expenses separately. As a sole trader or sole proprietor, your personal and business income is reported together for tax purposes, but keeping the transactions separate makes that reporting accurate and far less stressful.

Do I need a business bank account by law?

For registered companies, limited companies, LLCs, and corporations, yes, in most jurisdictions, this is either a legal requirement or a practical necessity tied to your registration obligations. For sole traders and sole proprietors, the legal requirement varies by country, but the practical requirement is universal: you need separate records to file accurate taxes and manage your finances effectively.

What is the fastest way to separate finances if I have been mixing them for a while?

Open the business account today and start clean from this moment forward. Then work backwards through your records one month at a time. Focus first on the current tax year. Use a spreadsheet or import your bank statements into a free tool like Wave to categorise transactions in bulk rather than one by one. If the backlog is significant, one session with a bookkeeper can often clear 3 to 6 months of messy records in a few hours -- the cost is usually worth it.

Conclusion

Separating your personal and business finances is not complicated, but it does require a deliberate decision to set it up properly. The seven steps in this guide, opening a dedicated account, getting a business card, paying yourself consistently, tracking expenses in one system, setting up proper invoicing, reconciling monthly, and cleaning up any existing mix, build a financial foundation that makes every other part of running your business easier.

Your bank statements become readable. Your tax preparation becomes straightforward. Your cash flow becomes visible. And instead of spending hours at year-end trying to reconstruct what happened, you simply open your books, and the picture is already there.

The business owners who avoid financial stress are not the ones who are better at maths. They are the ones who built simple systems early and stuck to them.

For a broader picture of your financial health across all five areas, take the free MoneyKoneKt Business Finance Health Check below. It takes 10 minutes and gives you a clear, honest score with specific next steps tailored to where your business actually stands.